The Month in Review - Aug 2022

Monthly Review

Farrow Hughes Mulcahy Investment Research 13 September 2022

Markets were varied in August with the MSCI World Index in $US down -4.1% and the ASX 200 Index rising 1.2%.

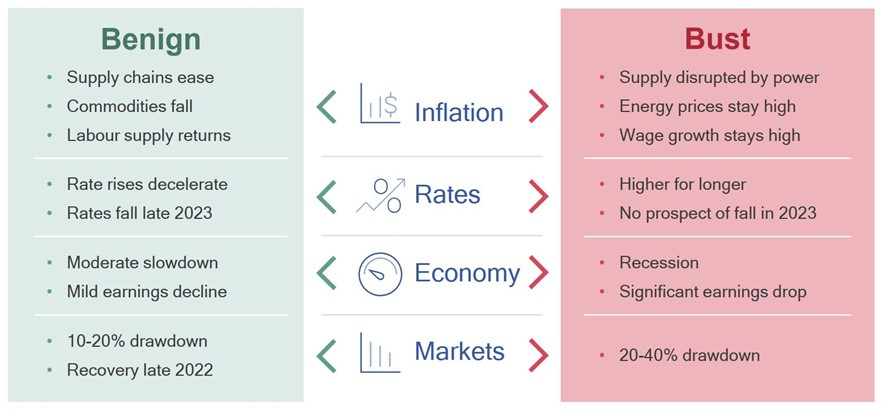

The market remains at a “sliding doors” moment between two potentially very different outcomes, shown here:

The market is like a pendulum swinging between the two outcomes. It is reacting badly to signals of more tightening, fearing a policy mistake will trigger a recession. It then swings more positively when data indicates the economy is more resilient and inflation signals are improving.

There has been a clear shift in the market’s view on monetary policy in recent weeks. It is now expecting more hawkish outcomes from central banks, pricing in a 75bp hike at the Fed’s next meeting, with rates peaking around 4%.

The RBA lifted the cash rate by 0.50% this week to 2.35% (as expected by economists), this was the fifth consecutive increase in interest rates since May. There was the obvious observation that as rates get higher, there is a rising likelihood of a slowdown in rate increases. But reference to the 2-3% inflation rate as a medium-term target was a more important dovish signal.

If central banks are prepared to allow inflation run a bit hotter for a bit longer, they don’t need to be as aggressive on the level of rates. This is what the market and the Australian government wants to happen. The RBA, under pressure and not wanting to be blamed for causing a downturn, appears prepared to oblige. There is some logic to this. Australia has had a lower consumption boom, higher savings and lower wages growth than the US. The RBA will be hoping that other central banks actions will ease global inflationary pressures, doing a lot of their work for them. A more benign rate cycle would be good for Australian equities relative to other markets.

The risk to this approach is that inflation doesn’t fall as quickly as hoped — and we are left needing to do more later. Interestingly this is the opposite approach of most other central banks, which are signalling they will be more aggressive sooner and front-end hikes.

Shares remain at high risk of further falls in the months ahead as central banks continue to tighten to combat high inflation, uncertainty about recession remains high and geopolitical risks continue. However, we see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year allowing central banks to ease up on the monetary policy brakes.

With bond yields looking like they have peaked for now short-term bond returns should improve a bit further.

Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

The $A is likely to remain volatile in the short term as global uncertainties persist. However, a rising trend in the $A is likely over the medium term as commodity prices ultimately remain in a super cycle bull market.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

Source: AMP Capital, Pendal Group, AZ Sestante.