The Month in Review - Feb 2023

Monthly Review

Farrow Hughes Mulcahy Investment Research 14 March 2023

Markets moderated in February after their strong start to the year. The ASX 200 was down -2.4% and the MSCI World $AU was up 2%.

Fed Chair Powell indicated that the peak level of interest rates is likely to be higher than previously expected and if warranted the Fed is prepared to step up the pace of rate hikes again. So far the economic data has been mixed and with the Fed likely to be wary following the regional bank failures it’s likely to stick to a +0.25% hike at its next meeting, rather than move back to 0.5%.

The collapse or closure of two regional US lenders – Silicon Valley Bank which was a lender to tech start-ups and Silvergate Capital which was a crypto friendly lender have led to concerns that they may reflect the start of broader problems in the US banking system. This is quite possible as Fed rate hike cycles by tightening financial conditions invariably trigger financial stresses (think the tech wreck and GFC) and troubles in startup companies and crypto businesses and nervous depositors in banks who fund them are not that surprising in this environment, given what’s happened to crypto over the last year. At this stage it’s too early to tell if problems at these lenders reflect just isolated problems or are indicative of wider potential problems impacting the US banking system. Either way banks are likely to see a tougher environment ahead as growth slows and higher rates cause more financial stress for borrowers. It is a sign that Fed tightening has got traction and the Fed may be close to the top on rates.

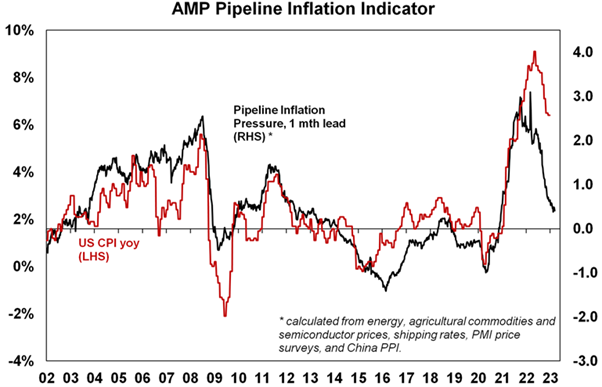

More broadly, our view is that the US economy will continue to slow – with most leading indicators including the yield curve still pointing down – and that this will flow through to a further slowing in inflation – with our Pipeline Inflation Indicator continuing to point down. Ultimately this should enable the Fed to stop tightening before triggering a deep recession, albeit the odds of a mild recession are high. And given the uncertainties share market volatility is likely to remain very high.

Source: Bloomberg, AMP

It was also a different story at the RBA, which in contrast to the Fed has become less hawkish. As expected, the RBA increased the cash rate by another 0.25% taking it to 3.6%. But thanks to a run of softer economic data the RBA wound back its hawkishness from last month that followed the stronger than expected December quarter inflation data. While it’s still hawkish and repeated its message on the need to get inflation down, it acknowledged recent data that showed slowing growth, some easing in the jobs market, signs of a peak in inflation and reduced risk of a wages breakout.

The year ahead is likely to see easing inflation pressures, central banks moving to get off the brakes and economic growth weakening but stronger than feared. This along with improved valuations should make for better returns than in 2022. But there will be bumps on the way – particularly regarding interest rates, recession risks, geopolitical risks and raising the US debt ceiling in the September quarter.

US shares are likely to remain a relative underperformer compared to non-US shares reflecting still higher price to earnings multiples versus non-US shares. The $US is also likely to weaken which should benefit emerging and Asian shares. Australian shares are likely to outperform again, helped by stronger economic growth than in other developed countries and stronger growth in China supporting commodity prices and as investors continue to like the grossed-up dividend yield of around 5.5%.

Australian home prices are likely to fall another 8% or so as rate hikes continue to impact, resulting in a top to bottom fall of 15-20%, but with prices expected to bottom around the September quarter, ahead of gains late in the year as the RBA moves toward rate cuts.

Cash and bank deposits are expected to provide returns of around 3.25%, reflecting the back up in interest rates through 2022.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

Source: AMP Capital, Pendal Group, AZ Sestante