It was a poor month for investment markets with the MSCI World Index Au down -3.3% and the ASX 200 falling -6.22%.

After falling back to around the June lows, shares were due for a bounce which we saw last week. However, the tech wreck and GFC bear markets saw several similar big 5%+ rallies (like in the last week) that proved short-lived, only to see the bear market resume. From a macro perspective, the risks for shares are likely still on the downside in the short-term as central banks remain hawkish, recession risks are high and still rising, the conflict in Ukraine looks likely to escalate, oil prices could move higher on OPEC’s move to cut oil production and earnings expectations are still being revised down.

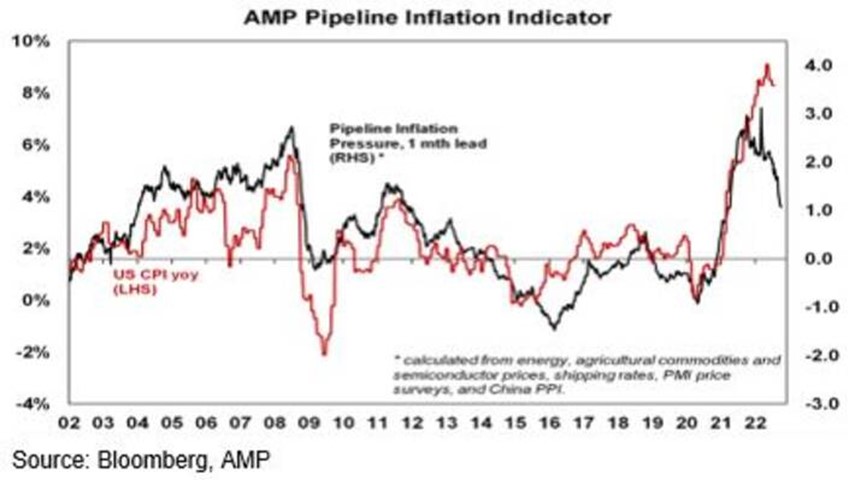

The good news remains that our Pipeline Inflation Indicator continues to slow reflecting improving global supply conditions and reducing corporate pricing power. We remain of the view that this, along with slowing economic conditions, will see inflation falling faster than central banks expect through next year. This should enable them to start slowing the pace of hiking from later this year.

The RBA has sensibly broken from the ultra-hawkish global central bank consensus and opted to slow the pace of rate hikes from the 0.5% to a more normal 0.25%. This made good sense given: the rapidity of the rate hikes so far; the need to better assess the impact of those rate hikes and in particular, allow for those on fixed 2% rates rolling over to rates two to three times higher next year; the greater sensitivity of Australian households to interest rate changes due to high household debt levels and a very high reliance on variable or short dated fixed rates (compared to 30-year fixed rates in the US); a bit of breathing space provided by lower wages growth in Australia compared to other countries; and the rising risk of global recession and financial turmoil. Of course, the slowdown in rate hikes does not mean that the RBA has finished hiking – it stressed that it “remains resolute” in returning inflation to target, will do “what is necessary to achieve that” and expects to increase rates further. We expect that the RBA will hike by another 0.25% in November or December taking the cash rate to 2.85%, which may be the peak, as a clear slowing in consumer spending is expected to emerge in the next six months.

Shares remain at high risk of further falls in the short-term as central banks continue to tighten, uncertainty about recession remains high and geopolitical risks continue. However, we see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year, allowing central banks to ease up on the monetary brakes.

With bond yields likely at or close to peaking for now, short-term bond returns should improve.

Unlisted commercial property may see some weakness in retail & office returns, plus the lagged impact of higher bond yields is likely to drag down unlisted property and infrastructure returns.

Australian home prices are expected to fall 15 to 20% top to bottom to the September quarter next year, as poor affordability & rising mortgage rates impact. (This assumes the cash rate tops out around 3%, but if it rises to 4% or more as the money market is assuming, then home prices will likely fall 30%.)

Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.