Australian equities rose around 6% for the month of November. Global equities were higher up 2.9%, with materials, industrials and financials outperforming whilst energy, healthcare, information technology and consumer discretionary underperformed.

US equities underperformed broader global markets (+0.6%) despite the Fed hiking in line with consensus, as expectation for future hikes softened following slightly weaker CPI and slowing economic data. European equities outperformed (+6.3%) despite the ECB and Bank of England hiking in line with expectations, with concerns relating to natural gas stores subsiding and further details on fiscal support addressing energy shortages released.

Asian equities were strong over the month (+10.2%), particularly Chinese equities (+15.8%) following the announcement of policy changes relaxing COVID-zero restrictions, with further easing expected. Positive sentiment in China was furthered by the Peoples Bank of China easing monetary policy and the announcement of further support for the property sector. Japanese equities were higher (+4.7%) as the Bank of Japan continued loose monetary policy while defending the Yen, this is despite signs of inflation marginally increasing.

There are six big macro issues going into next year:

1.The persistence of inflation — and how tight financial conditions will need to be in response

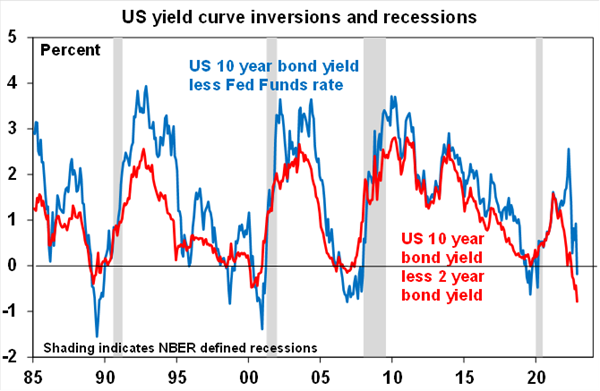

2.The scale of economic slowdown in the US and developed markets. (Real-time signals are benign, but the yield curve is a very negative signal)

3.The earnings leverage to that downturn — and whether nominal growth buffers earnings

4.Whether markets have already priced in economic downturn. The bear view is that markets bottom during recession, not before. Bulls point to a falling oil price, a weaker US dollar and lower bond yields as evidence of lessening headwinds for equities

5.What China’s economy does as it exits zero covid

6.Whether the RBA can engineer a soft landing in Australia

The main concern is the rising risk of recession in the US as this would drag down global and Australian growth and profits. The US yield curve has continued to invert and its business conditions PMIs are weaker than in other major countries and pushing near recessionary levels.

Source: Bloomberg, AMP

In fact, with recession risk in the US now high – it’s probably now up around 55% – and forward-looking price indicators easing there is now a strong argument for the Fed to pause interest rates on the grounds that a recession or significant slowdown will lead to much lower inflation ahead. On previous occasions when the Fed Funds rate rose above the 10-year bond yield in 1989, 2000, 2006 and 2019 the Fed paused rate hikes knowing that yield curve inversions often precede recessions. To continue hiking too far from here could risk a deep recession which invariably suppress inflation. So even if the Fed goes a bit further it’s looking likely we may be nearer the top than market expectations and the Fed’s dot plot for a rise to 5% indicate.

Shares are not completely out of the woods yet as central banks continue to tighten, uncertainty about recession remains high and geopolitical risks continue. However, we are now in a favourable part of the year for shares from a seasonal perspective and it’s likely to see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year allowing central banks to ease up on the monetary brakes.

With bond yields likely at or close to peaking for now, short-term bond returns should improve.

Australian home prices are expected to fall 15 to 20% top to bottom into the September quarter next year as poor affordability & rising mortgage rates impact. This assumes the cash rate tops out in the low 3’s but if it rises to around 4% as the money market is assuming then home prices will likely fall 30%.

Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

We take this opportunity to wish you a happy and safe holiday season and look forward to a successful 2023.

Source: AMP Capital Investors, Pendal.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.