The strong upward trend in Equity markets continued this month with International markets up 3.2% (MSCI world $Au) and the Australian market rising 1.6%.

US data remains strong with a 17-year high in consumer confidence, another strong ISM manufacturing conditions reading, solid growth in construction activity, strong gains in home sales, rising house prices and an upward revision to September quarter GDP to 3.3%. While the Fed’s Beige Book sees economic growth, wages growth and inflation as all being “modest to moderate” it did note widespread labour market tightness and skill shortages and Fed Chair Yellen noted broad based growth and that gradual rate hikes remain appropriate. With inflation in the core private consumption deflator rising to 1.4% year on year (or 1.447% to be precise), the Fed remains on track to hike again this month and three (or four) more times next year. Market expectations for the Fed remain too dovish.

Eurozone economic confidence rose to a 16-year high in November and unemployment fell again in October but core inflation remained low at 0.9% year on year keeping the ECB cautious.

Chinese data was solid with industrial profit growth remaining strong and business conditions PMIs remaining reasonable on average in November (with the Caixin PMI down slightly but the official PMIs up) suggesting that growth has remained solid into year-end. Measures aimed at reducing financial risk point to some softening in growth into next year though.

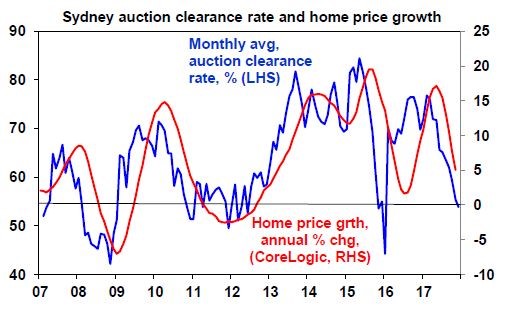

The Sydney and Melbourne property boom is fading thanks to APRA’s tightening measures (higher rates for investors and interest only borrowers, etc.), rising supply and weakening expectations. Sydney auction clearance rates have already fallen into the mid-50s, a level that points to price declines on an annual basis on the back of the experience in 2008 and 2012. (This didn’t happen in 2016 because the auction slowdown then was too brief.)

Source: Domain, CoreLogic, AMP Capital

Our view remains that average residential property prices in Sydney and, with a lag, Melbourne will fall 5-10% into 2019. Perth is bottoming and should start to see moderate price gains by 2019, with Darwin following too. Brisbane, Adelaide and Canberra are likely to see continuing moderate gains over the next few years with some acceleration possible and Hobart will remain strong.

While strong business conditions, solid jobs growth, improving global growth and the RBA’s own forecasts for a pick-up in growth argue for an eventual rate hike, at Tuesday’s meeting the RBA left rates on hold. We do not expect a rate rise in Australia until late next year at the earliest.

Below is a brief summary of our outlook for 2018 and a few things to keep your eye on.

Despite the usual worry list, 2017 has been pretty good for investors as global growth and profits accelerated and central banks stayed benign as inflation stayed low.

The “sweet spot” combination of solid global growth and profits and yet low inflation and benign central banks is likely to continue in 2018. However, US inflation is likely to start to stir and the Fed is likely to get a bit more aggressive. Expect a gradual rise in bond yields and a rising US dollar. The RBA is unlikely to start hiking rates until late 2018 at the earliest.

Most growth assets are likely to trend higher, but expect more volatility and more constrained returns. Australian shares are likely to remain laggards.

The main things to keep an eye on are: the risks around Trump; inflation, the Fed and the $US; bond yields; the Italian election; China; and Australian property prices.

We take this opportunity to wish all of our clients and their families a Merry Christmas and a safe and profitable New Year.