The Month in Review - January 2018

Monthly Review

Farrow Hughes Mulcahy Investment Research 05 February 2018

Equity markets were mixed during January with the Australian ASX 200 down 0.5% but International markets were up 5.2% (MSCI world $US). This continues last year’s trend in favour of International investment.

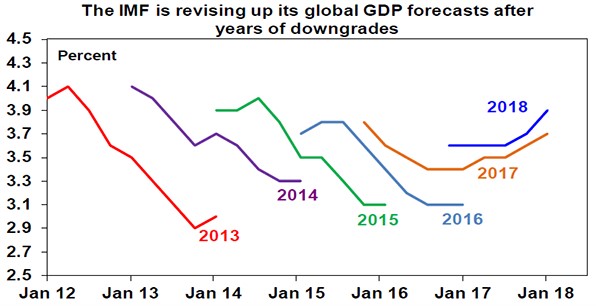

Global growth forecasts still being revised up. In its latest global economic review, the IMF revised up its growth forecasts yet again, with broad-based increases. The pattern of IMF revisions is basically the same as for private sector forecasters and as the next chart highlights years of growth downgrades have given way to upgrades as the post-GFC hangover has finally given way to more self-sustaining growth. Just as the growth downgrades were associated with falling inflation, ongoing monetary easing and falling bond yields the upgrades are likely to eventually give way to rising inflation, gradual monetary tightening and further increases in bond yields.

US economic data remains mostly solid. Home sales fell, but readings for January business conditions PMIs, durable goods orders, leading indicators and home prices were all solid. December quarter GDP growth was lower than expected at 2.6%, but this was due to detractions from trade and inventories with strong gains in consumption and investment. The December quarter US earnings reporting season is off to a strong start. Of the 133 S&P 500 companies to have reported so far, 81% have beaten earnings expectations and 82% have beaten on sales.

Meanwhile, Eurozone business conditions PMIs, the German IFO business climate survey and consumer confidence rose even further in January to very strong levels, which is consistent with a further rise in economic growth. The ECB’s December bank lending survey also showed stable or easing lending standards and rising credit demand.

The Bank of Japan made no changes to its monetary policy or its growth and inflation forecasts. While it noted that inflation expectations are no longer falling, it continues to see downside risks to inflation, and the one dissent was dovish. With core inflation stuck at 0.3% in December and way below target, no early exit from monetary stimulus is likely.

The Australian December half 2017 earnings reporting season will start to get underway but with only a trickle of companies including Navitas, GUD and James Hardie. Expect to see a fall back to single digit earnings growth (after the resource-driven surge seen in 2016-17) with overall earnings growth around 5%, with resources slowing to around 1%, banks around 3% and industrials up 8% with strong results for healthcare, gaming, building materials and consumer staples.

For 2018, ongoing strong economic and profit growth and still easy monetary policy should keep investment returns favourable but stirring US inflation, the drip feed of Fed hikes and a possible increase in political risk are likely to constrain returns and boost volatility after the relative calm of 2017. Apart from the likelihood of a correction early in 2018 and more volatility through the year, global shares are likely to trend higher through 2018.

Australian shares are likely to do okay but with returns constrained to around 8% with moderate earnings growth.

Commodity prices are likely to push higher in response to strong global growth.

Low yields and capital losses from a gradual rise in bond yields are likely to see low returns from bonds.

National capital city residential property price gains are expected to slow to around zero, as the air comes out of the Sydney and Melbourne property boom and prices fall by around 5%, but Perth and Darwin bottom out, Adelaide and Brisbane see moderate gains and Hobart booms.

Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.2%.

After reaching as high as US$0.8134 which is near the top of the technical channel it’s been in since 2015, the next big move for the A$ against the US$ is more likely to be down than up, as the gap between the Fed Funds rate and the RBA’s cash rate goes negative. Trump’s comment that he wants to see a strong US dollar should help. Solid commodity prices will provide a floor for the A$ though.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.