The Month in Review - February 2018

Monthly Review

Farrow Hughes Mulcahy Investment Research 06 March 2018

Equity markets were weak during February with the Australian ASX 200 barely moving but International markets were down 4.3% (MSCI world $US).

We remain of the view that the pullback in share markets seen last month is a correction as opposed to the start of a major bear market, but we may not have seen the last of February’s share market lows. With US inflation and Fed expectations still moving higher and Trump adding to the inflationary pressure in the US with tariff hikes, share markets are likely to remain volatile in the short term with a high risk of seeing a re-test of February’s share market lows.

Fed Chair Powell’s first Congressional Testimony was slightly hawkish. While Powell’s prepared comments were pretty balanced, his answers to questions indicated he wasn’t concerned about a bit of market volatility and that he is leaning to four rate hikes this year. Since the December Fed meeting, which had three hikes in the so-called dot plot, global growth and US fiscal policy have become tailwinds to US growth and confidence in the US outlook has increased.

The US December quarter earnings reporting season is now effectively done with profits up 16% for the year to December, earnings up 8% and expectations for profit growth this year revised up to 20.6%. This is very supportive of shares, beyond uncertainties around the Fed and bond yields.

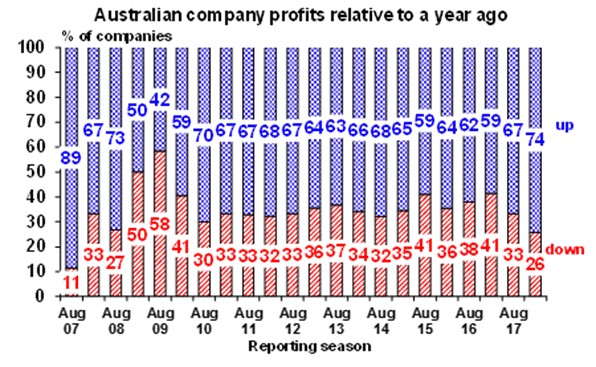

Solid broad-based profit growth with a good outlook will help the Australian share market, but it’s still lagging global profit growth. The profit reporting season for the December half is now done and has been pretty good. 46% of results have exceeded expectations (against a norm of 44%), 74% of companies have seen profits rise from a year ago (compared to a norm of 65%) which is the strongest since the GFC and 66% have increased dividends from a year ago, with 26% keeping them flat, which is a sign of ongoing confidence in the outlook. Reflecting the reasonable quality of results, 59% of companies saw their share price outperform the market the day results were released (against a norm of 54%). Consensus profit growth expectations for this financial year remain around 7%, with resources upgraded slightly to 16% and the rest of the market downgraded to 5% (from 6%) owing to a downgrade to banks. Profit growth expectations for 2018-19 have been upgraded to 5% (from 4%) thanks to resources. This is good news and will underpin a rising trend in the Australian share market. That said, local profit growth continues to lag global profit growth, where it’s running around 14%.

Volatility in share markets is likely to remain high and we may see a retest of February’s share market lows, with investors yet to fully digest the outlook for higher inflation and interest rates in the US, but the broad trend in share markets is likely to remain up as global recession is unlikely and earnings growth remains strong globally and solid in Australia.

National capital city residential property price gains are expected to slow to around zero as the air continues to come out of the Sydney and Melbourne property boom and prices fall by around 5%, but Perth and Darwin bottom out, Adelaide and Brisbane see moderate gains and Hobart booms.

Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.2%.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.