The Month in Review - Oct 2021

Monthly Review

Farrow Hughes Mulcahy Investment Research 09 November 2021

INFLATION concerns eased last week and there were implications for central bank messaging. There had been concern that higher inflation would prompt central banks to shift messaging more aggressively towards potential rate hikes. That seems to be allayed for now. This came via statements from central banks, a US labour report that indicated a return of supply, and a firmer chance that Jay Powell will be reappointed for a second term at the Fed.

Bond yields fell in response. In combination with a decent US earnings season and good news on Pfizer’s antiviral pill, the S&P 500 rose 2.03% and the S&P/ASX 300 gained 1.91% last week.

US equities have had a strong run, up 9.17% for the quarter. Australian equities have lagged, up only 2.02%. This reflects our skew to resources and the need to digest new capital issuance. While they might pause for breath in the near term, equity markets should remain supported into the year’s end.

Various statements from central banks went a long way to calming the market’s concerns about how quickly rates will need to rise. The Fed announced it would begin tapering asset purchases by US$15 billion per month, implying that Quantitative easing would end in mid-June 2022. This is in-line with expectations and was a dovish statement given speculation that the rate might have been accelerated. Chair Powell was at pains to talk down inflationary fears. He noted that “transitory” did not necessarily mean “short-lived” — rather they were not expecting “permanently higher inflation”, i.e., a wage-price spiral. They did give themselves room to adjust their plans.

The RBA also adjusted its messaging. The three-year yield target was removed as expected. The possibility of a rate rise in 2023 was also mentioned for the first time. The Reserve Bank noted that the labour market was stronger than expected but border re-opening should provide additional supply. This remains to be seen. The market is still wary of inflationary pressures, particularly in housing. Nevertheless, there was relief that the RBA didn’t take a dogmatic stance towards the target for a first hike in 2024.

The dominant narrative at this point is that global growth is accelerating following a hit from the Delta strain and disrupted supply chains. Bottlenecks persist but there are signs the situation is improving. This was reinforced by US payroll data, which showed 531,000 jobs were added in October, versus 450,000 expected.

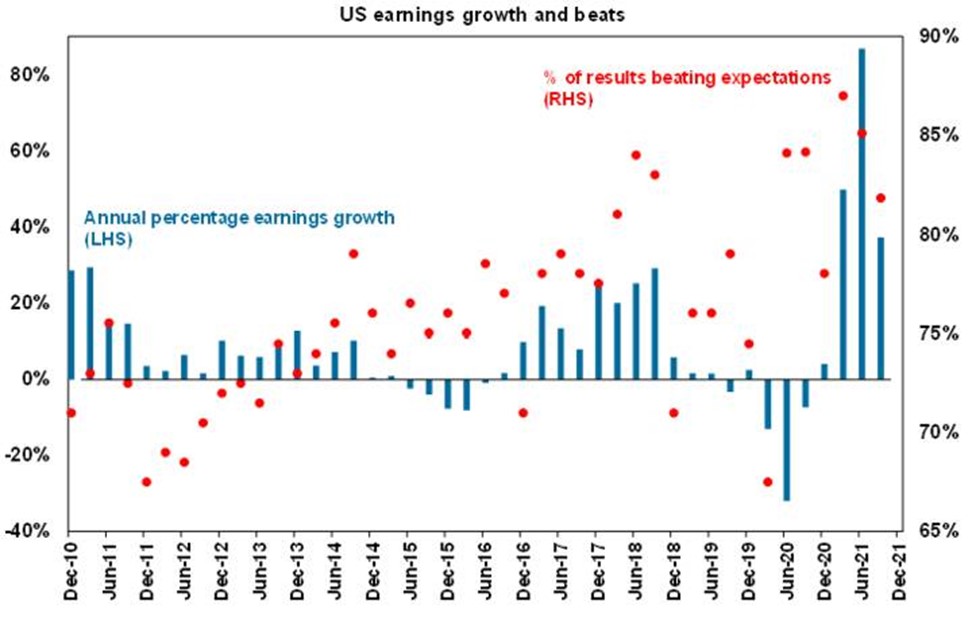

A positive US third quarter reporting season has been driving share markets higher. Nearly 82% of companies have beaten expectations which is better than the average long-run beat of 76%. Annual earnings growth has slowed to around 37% but this comes off the back of very strong earnings growth in recent periods and is well above the usual growth in annual earnings (see the chart below).

Source: Bloomberg, Credit Suisse, AMP Capital

Strong earnings and profit growth is occurring despite issues of higher inflation and supply chain problems which were mentioned a lot in the earnings results.

Shares remain vulnerable to short-term volatility with possible triggers being coronavirus, global supply constraints & the inflation scare, less dovish central banks, US fiscal plans and the slowing Chinese economy. But we are now coming into a stronger period seasonally for shares and the combination of improving global growth and earnings, vaccines allowing a more sustained reopening and still low interest rates augurs well for shares over the next 12 months.

Australian home prices look likely to rise by around 21% this year before slowing to around 5% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a further slowing in the pace of gains as poor affordability impacts, home buyer incentives are cut back, listings return to more normal levels, fixed mortgage rates rise further, and macro prudential tightening slows lending.

Cash and bank deposits are likely to provide poor returns, given the ultra-low cash rate of 0.1%.

Important note: While every care has been taken in the preparation of this document, Farrow Hughes Mulcahy make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

Source: AMP Capital. Pendal Group.